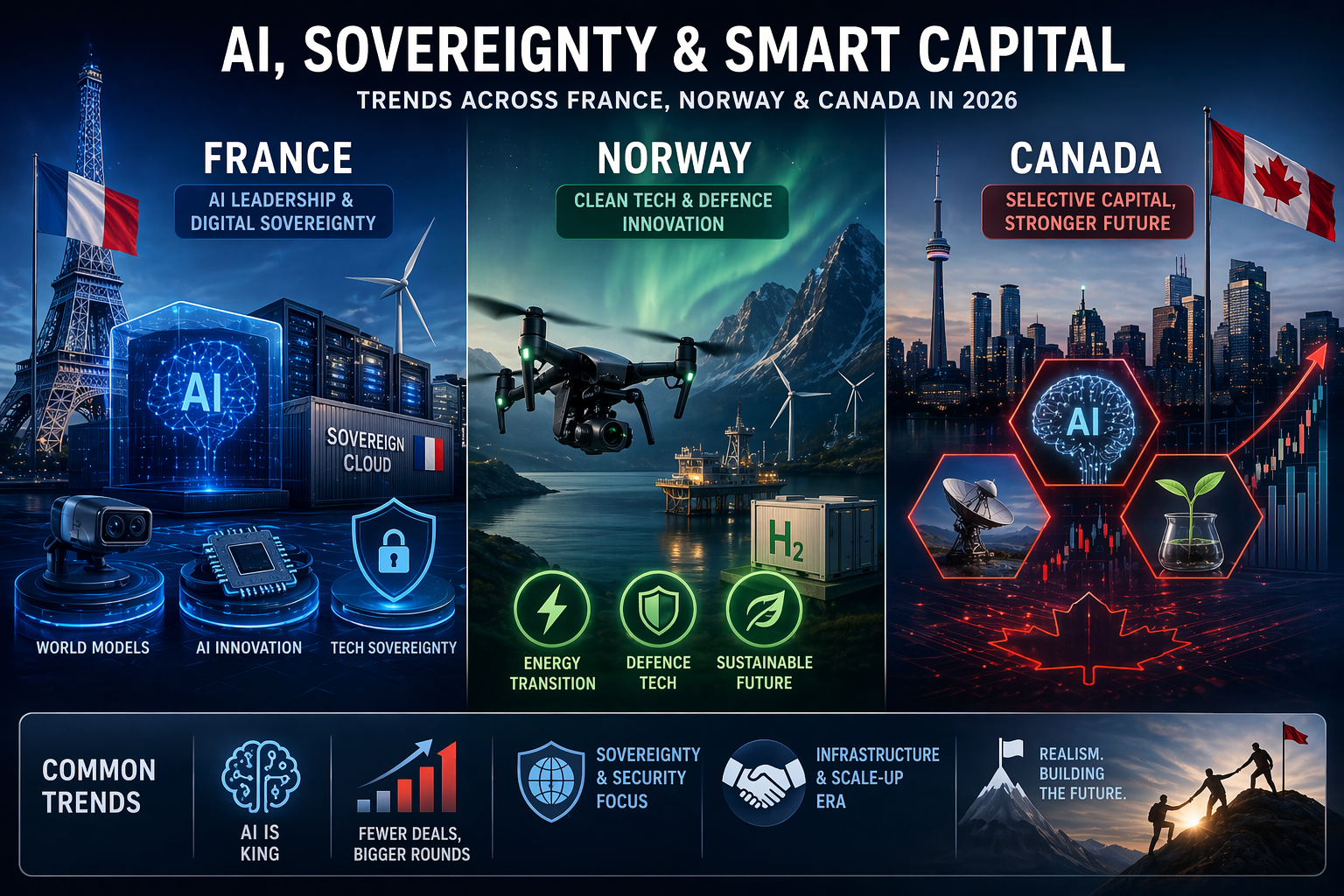

France: AI Dominance, Mega-Rounds, and Sovereignty Push France continues to lead Europe in AI and deeptech momentum, with strong VC activity despite fewer but larger deals. In Q1 2026, French startups raised €2.73 billion (up 79% YoY), though deal count dropped 27%, signaling capital concentration in top-tier AI plays.  • AMI Labs (founded by Yann LeCun, ex-Meta AI chief) raised ~€895 million (~$1.03 billion) in what’s described as Europe’s largest-ever seed round at a $3.5 billion pre-money valuation. The round, backed by Cathay Innovation, Greycroft, Bezos Expeditions, Nvidia, and others (including Xavier Niel), funds “world models” — AI that learns physical reality from video/movement as an alternative to traditional LLMs.

• Mistral AI secured $830 million in debt financing to build its first sovereign data center in Bruyères-le-Châtel, advancing French efforts toward tech independence from U.S. hyperscalers.

• AI now accounts for ~45% of French VC funding (up from 20% in 2020), driving the country’s outsized share of Europe’s fastest-growing companies (FT1000). Investors predict a defence tech champion emerging in 2026 alongside a shift away from pure “VC-first” models toward sovereignty-focused infrastructure.

• Broader trends: Public sector moves to reduce reliance on U.S. tech, plus programs like French Tech Rise to boost regional startups. New lists highlight 10+ promising 2024–2025-founded AI, deeptech, and materials startups to watch. On X, recent chatter touches on French tech bureaucracy slowing innovation (e.g., permitting for robotics) and Linux/open-source adoption in the ecosystem

Norway: Steady Climate/Deeptech Activity with Selective Funding Norway’s ecosystem remains more modest in volume but focused on sustainability, energy transition, and emerging defence/deeptech. YTD 2026 funding sits at ~$141 million across 16 rounds (down slightly YoY), with emphasis on high-quality, impact-driven plays.  • Stendr raised $5.4 million pre-seed for AI-powered drone detection systems (defence/tech security angle), backed by Rainfall, Startuplab, Antler, and ACME.  • Other recent activity: Zeabuz (Seed) and Lace Lithography (Series A) closed rounds, with investors like Grieg Kapital and Atomico involved. Energy storage innovator Photoncycle previously raised €15 million for “summer sun to winter power” hydrogen solutions.  • Top VCs (e.g., Skyfall, Hadean, Alliance VC, Innovation Norway) continue backing SaaS, cleantech, and life sciences. Oslo hosts many of the 69+ startups to watch in 2026, with unicorns valued at ~$5.7 billion collectively. Startuplab closed a $32 million fund to support early-stage Norwegian tech.  X discussions highlight Norway’s oil fund debates (EU interest in energy profits/taxes for Ukraine aid, though not a direct seizure proposal) and tech strengths in offshore/energy applications.

Canada: Selective Capital, AI/Defence Focus Amid Challenges Canadian VC remains cautious, with YTD 2026 funding at ~$1.96 billion across 116 rounds (down ~21% YoY in volume and sharply in deal count). Capital concentrates in resilient sectors like AI, defence, and climate tech amid U.S. trade tensions and reduced American investor participation (down to 25% of deals).  • PH7 Technologies closed a Series B, and FutureFit AI raised Series A, reflecting ongoing AI and enterprise interest.  • CIX Startup Awards 2026 named 14 winners (e.g., Qidni Labs in medtech, WeavAir in climate tech, plus fintech and defence plays) for their innovation in solving ‘hard problems’.

• Outlook for 2026: High selectivity, with AI as the top draw and defence/security boosted by federal spending. Cleantech faces caution. Scale-ups are emphasized as critical, alongside policy support for autonomy. U.S. investors pulled back in later-stage deals.  • Top VCs like Inovia Capital, Real Ventures, and OMERS Ventures stay active. Lists highlight 26+ startups tackling national challenges in a tougher funding environment.  On X, conversations cover CIX Summit networking, calls for more investment in gaming/media/consumer tech, and debates around subsidies, brain drain, and infrastructure.

Overall Trends Across the Three Markets • AI remains king: Heavy weighting in France and Canada; Norway leans more toward applied energy/defence tech. • Concentration effect: Fewer deals, bigger rounds for proven or sovereign plays. • Geopolitical angles: France pushes digital sovereignty; Canada navigates U.S. relations; Norway balances energy wealth with EU/Nordic dynamics. • Optimism with realism: 2026 is seen as a year for infrastructure buildout and scale-ups rather than hype

Filed in AI

How did this land?